By: Nate Bek

Take a tour of Seattle’s active venture firms, curated by Ascend.

By: Nate Bek

Take a tour of Seattle’s active venture firms, curated by Ascend.

Browse our collection of photos from Founders Bash 2024! :-)

By: Nate Bek

Talk to any startup expert about building the next Silicon Valley, and they’ll often point to one key element: a strong pipeline of seasoned advisors.

Startup advisors are trusted guides who bring wisdom and insight to the ridiculously tough journey of building a business. They offer strategic advice, share hard-earned lessons, and provide mentorship that goes far beyond simple guidance. Advisors are sounding boards for ideas, connectors to crucial networks, and steady hands in times of uncertainty. A great advisor can be a kingmaker.

For those in big tech or engineering roles outside the startup ecosystem, breaking into advisory roles can be challenging — there can be broad gaps between the networks of people who’ve spent their careers in companies that have already scaled, and those of serial entrepreneurs and startup founders.

Typically, these gaps are filled by institutional matchmakers — programs designed to connect founders with aspiring mentors.

In Seattle, Techstars served as one of those intermediaries. It brought together tech leaders, former founders, and investors. Its final “Mentor Madness” event paired 211 mentors with the 24 startups in its cohort, and nearly 350 mentors were listed on its website. No other local program operates at that scale today (although Foundations aims to help fill that void).

Techstars excelled at transforming casual introductions into lasting advisory relationships, helping a number of Seattle startups grow. The program provided structure and guidance for mentors, supported by resources like David Cohen’s Mentor Manifesto.

Now, with Techstars out of Seattle, the way startup advisors connect with founders has slowed.

The shift raises a big question: How do we continue to support the Seattle startup ecosystem with a steady flow of new advisors?

We’ve created an FAQ for big tech professionals interested in upholding the region’s robust mentor network. We gathered insights from both seasoned and emerging advisors.

Here’s what we learned:

Advising startups offers a chance to stay at the cutting-edge while sharing valuable experience. For many, it’s about being part of the journey, helping others overcome challenges, and staying connected to the pulse of new ideas and technologies.

Advisors are rarely in it just for the money, though equity packages and cash compensation are common.

Taylor Black, a Director on Microsoft's Incubation Studio & Strategic Programs Team and former B2B SaaS founder, says he’s driven by the thrill of working with early-stage companies.

“I love the zero-to-one space, getting from idea to product-market fit and all the questions that come with it,” he says.

With experience in deep tech, consumer, and platform technologies at Microsoft, Black has guided hundreds of startups through those critical first steps. The motivation is the excitement of turning ideas into reality and solving the puzzles that come with it.

David Pitman, a former staff engineer at Google Cloud and exited founder, says advising is about giving back.

“I got a lot of great mentoring and advising when I was a founder,” he says. “Some of those people are still my mentors today.” It’s a way to pay it forward, sharing hard-earned wisdom and staying connected.

Pitman adds that advising can be a two-way street: “You can rapidly build up a lot more knowledge about, say, how the current funding environment is going.”

Aseem Datar, vice president of next-gen computing and AI platform at Microsoft and a former Madrona Partner, says it’s important for you to find “advisor-founder fit.”

Stage: Figure out which stage of the startup’s lifecycle best fits your skills. If you’re like Black, that’s at the very early stages when the company is developing a product. But for others in big tech, it might make more sense to work with a later-stage company that found product-market fit and is looking to scale.

Value add: Determine the types of problems a founder might have, and how your unique skill set fills that gap. This could be customer intros, technical advice, supply chain support, culture and internal processes, and more.

Goals and financial situation: Some startups don’t have the cash on hand to pay you right away, or at all. Others might want to pay you and not want to give you equity for your help. The ideal situation is a mutual agreement with the founder and a genuine desire to help, which rewards a secondary bonus to you “picking up the shovel” and actually helping the startup grow.

Jim Alkove, founder of a cybersecurity startup and advisor to several others, says that you should start with determining your “why:” What do you want to achieve? And where can you offer the most value?

Black’s advice is straightforward: “Go for it, but be honest about what you’re good at. If you haven't built something from zero to one, don’t advise on that. Instead, focus on what you really know — whether that’s Kubernetes, C++, or setting up strong dev environments.”

Becoming an advisor is much like finding a new job. Begin by building a strong network and offering your help before officially taking on an advisory role to establish your value.

Connections with venture capitalists and startup studios can increase your visibility to startups. In relationships to both founders and their investors, offer customer introductions, even for companies you don’t plan to work with long term. Also offer your expertise as a trusted third-party reference. Alkove notes that he spends a significant amount of time on quick reference checks and technology due diligence, sometimes more than on customer intros.

He adds that his portfolio of advisory roles came from three key sources:

Echomark: Had an existing relationship with the founder, a former colleague at Microsoft.

Safebase: Spent time with the team and offered help, eventually joining as advisor.

Ambit: Was introduced through his relationships with venture capitalists.

Alkove says the most important aspect is spending time with the team. Understand their culture and product to see where you fit in and jump on opportunities to help.

There are also existing programs that you can join that serve as intermediaries:

For hardware-focused startups, Amish Patel launched Conduit Venture Labs’ Fellows. Taylor Black is a fellow there, and I wrote the story for GeekWire here.

For women-led companies, Seattle-based Graham & Walker has its Catalyst program (Jen Haller and I participated as mentors in its most recent Cohort).

When pitching yourself as an advisor, avoid positioning it as a pay-to-play network. Customer intros are important but should be done thoughtfully and with credibility. They should also be just one of many tools you offer to founders.

For Alkove, his value lies in his CISO connections. As a former executive at Salesforce, he was the buyer of cybersecurity tools, which enabled him to advise on how product pitches would be received.

“If you’re the ideal customer profile, that's valuable,” he says.

Pitman, drawing on his experience from Google Cloud and multiple startups, highlights the broad applicability of lessons learned in building from zero to one and thousands to billions.

His experiences with software, UX, and AI can help new tech companies avoid costly mistakes they have to unravel after they start rapidly growing post-Series A.

“The advantage of an advisor is having someone who can help you see ahead to the next stage of your company before you get there, basically giving a superpower to see into the future,” he says.

However, he cautions against applying big tech solutions to startups without considering their practicality. “If you can't come up with a realistic way that some small startup is going to be able to put your advice into action, it's probably not that useful for them,” he says.

Black combines his founder experience and legal background to excel in the zero-to-product-market-fit stage. He has worked in three venture studios, launching startups in deep tech, consumer tech, and platform at Microsoft. Black focuses on testing, ideation, and gathering data for product-market fit. He also uses his legal expertise to craft B2B contracts, which are crucial for refining a product and achieving product-market fit.

Programs like Conduit Venture Labs' Fellows program works with tech leaders to help hardware-focused startups avoid common pitfalls such as high burn rates, supply chain issues, and limited venture capital interest.

When diligencing startups, start with traditional factors: market potential, team background, product viability, and investors. These metrics provide a foundation, but to achieve advisor-founder fit, Pitman looks deeper into his relationship with the founder and the practicality of their professional alignment.

“I really want to understand as rapidly as possible if I can actually give useful advice,” he says. Pitman is cautious of founders who claim everything is perfect. “If you think your startup is doing great, you either got that lottery ticket—congrats—or, like most founders, something is always going wrong.”

To test the relationship, Pitman offers a small piece of advice early on and watches how founders respond. “I want to know this is going in a productive direction and not just giving advice that goes nowhere,” he says.

But Pitman is careful not to overstep: “I’d be more concerned if a startup took my advice without seeing it as one data point among many.”

Most enterprise professionals seek engaging and interesting opportunities outside their day job, with equity and cash often being secondary concerns—or not a concern at all. Their main motivation is to participate in something exciting beyond their regular work.

Many advisory engagements don't involve equity, especially when facilitated through platforms like incubators. Black, for example, offers startups around five one-hour sessions initially. After that, he prompts them to decide whether to formalize the relationship.

The choice between equity and cash depends on the advisor’s goals and the length of the engagement. Black advises opting for equity in long-term engagements due to its potential and crisp alignment with the startup's own fortunes. For short-term projects or one-off contributions, cash might be more practical. In early-stage startups, particularly those transitioning from zero to one, equity is often preferred over cash given the startup’s limited resources.

Equity pricing can be difficult to standardize, but resources like the Founder Institute’s FAST template provide a framework. An advisor dedicating at least 20 hours a month to an early-stage startup might expect around 1% equity.

Best practices start with connecting deeply with the team. If you’re a tech expert, engage with the engineers. Understand their challenges. Your job is to answer questions and ask the right ones, exposing areas for growth. Think of it as being on a board, but without the voting power.

Stay “operationally disconnected.” Offer advice with phrases like, “If I were in this situation…" Founders will make mistakes — let them. The key is to help them learn from those mistakes without stepping in too much. As an advisor, your main job is to provide input and ask good questions, which can expose areas that the founder can focus on developing. Be socratic but also supportive.

“It’s important to let go of your ego when becoming an advisor — empathy and experience result in the best wisdom,” Alkove says. “In the end, it can be a voyage of personal discovery and growth.”

Your pitch as an advisor should be about the full spectrum of value you provide, not just access.

Pitman brings lessons from extreme sports to advising. He knows the importance of realistic advice. The goal is to help founders push beyond their comfort zones.

“You want them to get to the next stage, so offer your expertise to help them achieve that,” Pitman says. “Talent only takes them so far.”

Nate Bek is an associate at Ascend, where he screens new deal opportunities, conducts due diligence, and publishes research. Prior to that he was a startups and venture capital reporter at GeekWire.

Disclaimer: The information provided here is for educational and informational purposes only. It does not constitute financial advice, and you should always consult with a qualified financial professional before making any investment decisions. Past performance is not indicative of future results.

By: Nate Bek

TX Zhuo’s path into venture capital began in the trenches of entrepreneurship. He built a company from scratch, scaled it to $10 million in revenue, and exited — all without a dime of VC funding.

“We made many mistakes along the way,” TX tells Ascend. This experience became the catalyst for his next chapter. “I told myself that if I ever were fortunate enough to sell my company, I would want to be a coach to other seed-stage entrepreneurs that might benefit from the lessons I learnt in my own journey.”

Today, TX is a General Partner at Fika Ventures, a Los Angeles-based seed-stage fund. Fika's focus spans financial technology, enterprise software, healthcare IT, applied AI, and marketplaces. Its sweet spot includes companies showing early market traction, just shy of product-market fit.

Fika raised more than $300 million across three flagship funds and one opportunity fund. Its portfolio includes Patrick Thompson, former co-founder and CEO of Iteratively, a Seattle startup co-invested with Ascend and later acquired by Amplitude.

TX and his team are selective about the startups it backs. “We try to be high conviction investors and limit ourselves to 8-10 investments so that we can dedicate enough time to each company,” he says.

This approach lets each portfolio company receive the attention it needs to thrive — that attention TX wishes he had while building his company.

Fika’s commitment to founder education extends beyond investments. The firm recently launched “Pour Over,” a podcast sharing insights and stories from founders and investors.

TX was kind enough to sit down with Ascend for our VC profile series, where we showcase early-stage investors from across the US. We talked in more depth about his journey into VC, Fika’s investment priorities and approach, and his cadence as an investor. Read to the end for carve-outs.

*We've edited this conversation for brevity. Enjoy! — Nate 👾

Nate: Thanks for chatting with us, TX. What made you decide to be a professional investor?

TX: I was a founder before and never managed to raise any venture capital. Although it was a moderately successful exit, we made many mistakes along the way (most could have been avoided if we had the right mentorship). And I told myself that if I ever were fortunate enough to sell my company, I would want to be a coach to other seed-stage entrepreneurs that might benefit from the lessons I learnt in my own journey.

What did you do before becoming an investor and how does that benefit your founders?

I took a break from college to start an online textbook marketplace and scaled it to more than $10 million in revenue and, after four years, got it to a successful exit. Thereafter, I spent a couple of years in management consulting (I know, many have said I took a step back in my career).

But I think the combination of experiencing the founder journey myself and benefitting from the structured thinking management consultant has provided me puts me in a good position to provide measured counsel to my companies (or at least that’s the hope!).

Why should founders want you on their cap table?

Speak to our other founders! Whenever we try to win a deal, we offer up the list of more than 80 companies we have backed, and prospective founders are more than welcome to speak to anyone of them.

What we promise is a very consistent, strong value-add approach where we are an extension of your management team instead of forcing our opinions on you. We make ourselves available whenever you need us but are not overbearing. And finally, we double down on the few things that really move the needle for you, namely customer introductions, talent referrals and problem solving leveraging our experience as founders before.

How many new pitches (actual calls/Zooms) do you take per month?

Two-to-three a day or 50 a month is probably a close estimate.

What’s your sweet spot(s) in terms of check size, valuation, and vertical?

$1-5 million pre-Series A investments, typically in the sub $20 million valuation range.

I would describe our ideal entry point as when companies show early market interest for their product (one stage before product market fit). Specifically, this is when a company has a product in market, a few early or beta customers that really love the product as it solves a high value, strategic problem for them.

As a firm, we focus on the following verticals – fintech, enterprise software, healthcare IT, applied AI and marketplace. I specifically lead our investing in fintech and vertical SaaS companies.

We try to be high conviction investors and limit ourselves to 8-10 investments so that we can dedicate enough time to each company. What this means is that the default is to lead every deal we invest in, but we are also conscious of being collaborative to make exceptions as the need arises.

How many new investments do you make per year?

8-10 as a firm

How do you stay informed about emerging markets and industries, particularly outside of Silicon Valley?

There is no replacement for time investment. We ensure that we visit geographies we care about outside of Los Angeles at least once a month so that we get assimilated into the local ecosystem and make a concerted effort to know the key stakeholders through dinners and events.

Like other members on my team, I spend at least 2-3 hours a week reading up and listening to podcasts that are relevant to the sectors I cover namely fintech and vertical SaaS so that we understand where the puck is moving and can provide well-informed advice/investment perspectives. I would say that this has been something that we have prioritized at Fika over the last 2-3 years such that at least 50% of our investing these days is thesis driven.

What factors influence your decision to invest in a new geographical area, like Seattle?

The supply-demand balance in terms of founders versus capital providers and whether there is a need for investors like us where we can actually add value. Seattle has all the ingredients to support a vibrant B2B startup ecosystem and that’s Fika’s direct focus. And even though there has been a birth of several amazing seed funds like Ascend in the last few years, there is still the lack of early-stage institutional capital in Seattle. We hope that Fika can play our part in filling that gap in the ecosystem.

What's your bull case for Seattle/PNW startups? On the flip side, what concerns should the region’s founders and investors keep in mind?

Huge amount of technical talent especially in the B2B space coming from successful companies like Amazon and Microsoft. More importantly, many of them have experienced scaling a company and that is vital when they become execs at fast-growing startups.

The irony of having successful startups in your backyard is that it always offers a compelling alternative for founders and talent in general. It is always easy for a founder to go back to work for one of these large companies or talent to stay in their cushy well-paying jobs. So I would say that community building such as joining a startup or starting a company is one of the top choices for everyone.

What’s your take on the key differences in the tech scenes of Silicon Valley and Seattle?

Seattle still feels extremely collegial in nature where investors are collaborating on deals and founders and rooting for one another. Not to say that Silicon Valley’s DNA is completely different, but Silicon Valley has gotten too large for these dynamics to exist.

What song is currently getting the most run on your Spotify/Apple Music?

Forever Young (all the different remixes) – seems to bring me back to my teenage days whenever I listen to the song.

Favorite shoes?

Jordan 1 Low Obsidian Ember Glow (and all Jordan 1 Lows for that matter).

What's your go-to ingredient in the kitchen, and do you think cooking and investing have anything in common?

I can’t cook! But I added spice to most of my meals so my kitchen is filled with all kinds of spicy sauces from red cut chili to Sriracha.

Patience and structure are key – I’m not a great cook (or a cook at all) as I’m impatient and don't follow instructions well. Guess that’s the same as running a company, you need to be patient and there are no shortcuts for success

Anything to add?

More co-investments with Ascend and other folks in the Seattle ecosystem, please!

More than 100 of our founder and investor friends made the 2.5-mile sprint, jog, or walk around Greenlake to pitch their startup or fund, part of Seattle Tech Week 2024 festivities.

Here’s our favorite moments from that early morning — captured in collaboration with Madrona.

By: Nate Bek

Seattle's startup scene is growing, but it’s clear we have some work to do.

That was a main takeaway from our panel discussion last week featuring venture capitalists from top-tier firms including Brentt Baltimore of Greycroft, Victoria Treyger of Felicis, and Sunil Nagaraj of Ubiquity Ventures, moderated by Kirby Winfield. Their goal: analyze Seattle's startup landscape from an outsider’s perspective with active Seattle investments.

They see a city rich in technical talent but with several missing pieces. Go-to-market strategies often lag behind technical capabilities; capital is available, but frequently from outside the region; and stronger community cohesion is needed to bridge incumbent tech leaders with founder types.

Here are our five favorite quotes from the panel:

Go-to-Market Strategies:"Seattle founders, in general, are not as strong in go-to-market strategies or storytelling," said Victoria. Improving these areas are key for growth.

Practical Valuations: "In Seattle, you have more practical, down-to-earth people and more practical valuations," said Sunil. This approach leads to better outcomes.

Community Cohesion: "There seems to be this divide between the incumbent tech community and the non-incumbent, newer people," said Brentt. Bridging this gap can strengthen the ecosystem.

Founder modesty: “People are just nicer here,” said Sunil. “In the Bay Area, there's a sense of entitlement and puffing up, especially with incubators like Y Combinator cultivating a culture where being a jerk is almost expected. That doesn't happen in Seattle. Here, it's nice, nerdy people working together.”

Accelerators: Seattle needs a stronger accelerator layer, similar to Y Combinator, to help founders get early customers and build effective go-to-market plans, Victoria said.

Keep reading for the full transcript.

*We've edited this conversation for brevity. Enjoy! — Nate 👾

Kirby Winfield: I'm Kirby Winfield, founding general partner of Ascend. We focus on pre-seed investments, primarily with Seattle founders, and specialize in AI, data, vertical software, and the horizontal AI that supports these companies. I'm thrilled to have friends from California here today.

Brentt Baltimore: I'm Brentt Baltimore from Greycroft. Thanks for having me; I'm excited to be here. I've been with Greycroft for about eight years, starting in our New York office and then moving back to LA. Greycroft is a 19-year-old firm with offices in New York and Los Angeles, and we added a San Francisco office just under a year ago. I focus on data and applied AI. Our most recent investment in Seattle is Groundlight. Our oldest investment in Seattle is Icertis, which is now much later stage.

Kirby: A little known fact about Greycroft, Dana Settle, the founding partner, I went to high school with her. She’s a Seattle local and also a University of Washington alum.

Victoria Treyger: I'm at Felicis and have been with the firm for almost six years. We focus on seed and Series A, across all sectors. We specialize in B2B, AI infrastructure, and AI applications. I've also worked on financial software, like the office of CFO, fraud, identity, and health tech.

One unique aspect of Felicis is our global investment approach. We're based in the Bay Area, but some of our best companies, like Adyn (Netherlands), Shopify (Canada), and Canva (Australia), are from all over the world. It will be interesting to compare lessons from these ecosystems to Seattle's.

Our main Seattle investments are more recent, within the last two years. They include MotherDuck, a phenomenal company, and a cool AI infrastructure company called Predibase (co-founder Travis is based here). We also invested in Atlas Health and have a recent, yet-to-be-announced investment in Seattle.

Sunil Nagaraj: My name is Sunil Nagaraj, and I'm with Ubiquity Ventures. Ubiquity is my own small VC firm. I call it a nerdy and early venture capital firm because I love to code and focus on products and first pitches. I do about 1,000 pitches a year and have invested in about five companies here over the years.

While at Bessemer, I sourced Simply Measured and Auth-0. Under Ubiquity, I've invested in ThruWave, Esper, and Olis Robotics. I love Seattle and first got introduced to the city in 2003 when I interned at Microsoft as a PM. I fell in love with the city and visit as often as I can.

At Ubiquity, I focus on software beyond the screen. I use my current $75 million fund to write checks between $1 and $2 million for companies taking software off computers and putting it into the real, physical world. Some of my investments include software on cows, in space, in our ears, and in field devices. I tend to move quickly because I work alone. For example, with Auth-0 in 2014, it took just seven days from meeting the company to committing to their seed round, which grew into a $6 billion company in Seattle.

Kirby: So let's dive in. We'll start with a softball question to get everyone in a good mood, and then we might move on to more controversial topics. To kick off, what do you like about Seattle founders or teams? What unique qualities do you find in this ecosystem, given that you all invest in many different regions?

Brentt: What I love the most about Seattle is the amount of technical depth. Even years ago, when I first started building relationships with founders and folks operating some of the bigger companies here, I noticed this. Coming from LA and spending most of my time in data, the technical expertise here really stands out.

As a firm, we focus on go-to-market strategies and spend most of our time supporting our portfolio companies in that area. The strong technical foundation in Seattle creates a perfect marriage for us.

Victoria: I'll add one more point, which I think is both a positive and an opportunity. Seattle founders tend to be more humble than founders in some other areas.

Kirby: Does that lead to opportunities for investors coming in the market, like pricing? Is there more value to be had here? Sometimes maybe other markets, or is that not a consideration?

Victoria: In the end, venture is a business of outliers. You're trying to find the Auth-0s and MotherDucks, the massive exits. That's really what you're looking for. Whether you're paying a 15 post or 20 post for a seed, you pick the very best founders and companies. It doesn't matter.

Sunil: I agree with everything you said. I would add that Seattle has its own strengths. I'm an emotional person, and I work alone, so I really vibe with my founders. People are just nicer here. In the Bay Area, there's a sense of entitlement and puffing up, especially with incubators like Y Combinator cultivating a culture where being a jerk is almost expected. That doesn't happen in Seattle. Here, it's nice, nerdy people working together.

When I think about founders, they're super nice, down-to-earth, and genuine people. They're about getting stuff done, not about showing off or projecting an image. I love that folks here are more humble and down-to-earth.

I do think you get more reasonable valuations here. In Seattle, when you raise money, you leave more room in your valuation for bumps along the way. In the Bay Area, if you raise at a 25 pre and then 30 pre, there's not much room for error over the next 12 months. Any hiccup can lead to a down round, which is really annoying for many reasons.

In Seattle, you have more practical, down-to-earth people and more practical valuations. VCs still buy about the same percentage, around 20% at each round, but it's more like buying 20% of a $2 million round instead of a $5 million one. This leads to a more enjoyable process and can still result in outlier outcomes like we've talked about.

Kirby: Let's explore the cultural differences between founders, keeping in mind that we're generalizing. We know there are exceptions, but for discussion's sake, let's handle this topic generally. Some founders out here might be seen as more humble. This can be viewed positively or negatively. What are some positive and negative differences between a typical founder here and those in New York or the Bay Area?

Victoria: From my perspective, Seattle founders, in general, are not as strong in go-to-market strategies or storytelling, including engaging with the press. This is a generalization, so take it with a grain of salt. Our firm has invested significantly in Australia's ecosystem and seen incredible outcomes. I have three investments there, and my partner Wesley has two, including Canva.

Australia, to be honest, has one massive company, Atlassian, which has spun out all three of my investments. Seattle has Amazon and Microsoft. The biggest difference I've noticed is that Atlassian founders are very scrappy and GTM-focused from the start. By the time we led the seed rounds, they already had early revenue and customers without significant marketing spend. They know how to gain traction in a scrappy way, which I don't see as much with Seattle founders.

Kirby: Do you think there's something about founders who spin out of recently parabolic startups that have become great companies? When the growth amplitude within the last 10 years has surged from, say, $10 million to $1 billion, are those founders closer to the early journey? Are they more likely to have those scrappy, GTM-focused characteristics than someone coming out of Apple, Google, Amazon, or Microsoft?

Brentt: I see it a bit differently. There is no shortage of technical talent willing to take the risk of starting something new. However, there seems to be a shortage of go-to-market talent willing to take that same risk and leave bigger companies. We don't see as many CROs, COOs, heads of go-to-market, or GMs from rapidly scaling companies or large corporations like Microsoft or Amazon leaving their roles as quickly as technical talent. There's a gap in risk appetite.

Kirby: I think that's been the criticism for some time. While I might be a bit self-interested or close to it, I do see this changing as we create more successful outcomes. We now have more people who have been recently involved in growing companies. Ten years ago, it was almost impossible to hire a marketer in Seattle for a startup with fewer than five people—they just kept rotating through the same ten jobs. It's gotten better, but the criticism remains valid.

Sunil: There's a massive difference between going from zero to one versus being at a large company like Amazon or Google. At a large company, you have stability, insurance, a good salary, and, importantly, distribution. For example, when Microsoft launches a new product like Teams, they can leverage their existing customer base and automatically include it in an Office 365 subscription. This built-in distribution is a huge advantage for go-to-market efforts.

In my pre-seed deep tech investing, I think a lot about the spectrum between "look what I built" versus "look who cares." Building new deep tech innovations is challenging—you need advanced expertise and careful thought. However, communicating the value to customers is different. It's not about the technical specs but about how it benefits the user, like getting someone promoted at their job. This mindset shift is crucial.

If you come from a large company, you may not have exercised the zero-to-one distribution skills needed for startups, which are very different from scaling an established product. This reflects the talent gap, where only a few executives become the go-to experts for go-to-market strategies. This issue has been noticeable in my experience, where a handful of executives rotate as the "kingmakers" of go-to-market.

Kirby: What would it take for you guys to be pounding the table in Seattle 5-10 years from now?

Sunil: The real issues are capital and skills. These two are interconnected. Events like this can attract more people, which brings mixed feelings. More competition for us in Seattle deals, but overall, it's positive to have investors look beyond the Bay Area.

New York had a consumer vibe, but it's now more general. Seattle has strong technical and SaaS depth, which is very attractive. Most investors don't frequently visit Seattle events, even though it's an easy trip. Promoting more capital in the area is important. We have great firms in Seattle, and while more capital might bring competition, it's beneficial for the ecosystem overall.

Kirby: Nate recently did the research, and more than 90% of the venture capital in this market comes from outside Seattle. We always tell founders that while we hope they can raise funds from one of our few local series investors, these investors simply don't have the capacity to support all the founders. The numbers clearly show this.

You mentioned that most VCs don't think of this market. I always tell this story: when I was raising for my first CEO gig around 2009, I spoke to a big multi-stage investor who said, "Oh, you're from Seattle. They don't work that hard up there, do they?" Hopefully, this attitude has changed with some recent successful outcomes, but misconceptions still linger. Even recently, I've had conversations where people say they don't want to leave their current location because there's plenty of opportunities there.

What are some misconceptions that folks in California or other areas might have about this market, especially secondary markets like Seattle?

Sunil: You've already pointed out one major misconception: the number of large exits. For example, Seattle has had five exits over $10 billion, which isn't widely publicized. Another misconception is about the talent pool. Some people think, "You can start there, but eventually, you'll have to move because there won't be enough talent to scale." This is a myth as well.

If we can gather and promote data to counter these misconceptions, it would be huge. Addressing these two big objections—whether there are real exits in Seattle and if there's enough talent to scale—can significantly change perceptions about the market.

Victoria: One thing missing in Seattle is a stronger ecosystem like YC, which focuses on acceleration. Despite the criticisms of YC, they excel at helping founders get early customers, build GTM plans, and get off the ground. When I looked at some TechStars companies here, I didn't think they provided the same level of acceleration. Pioneer Square Labs feels more like an incubator.

That accelerator layer is missing here, which ties back to the go-to-market piece. Building such an accelerator would be exciting for Seattle's amazing entrepreneurs. Interestingly, there are now 160 YC founders in Seattle, all connected through a WhatsApp group. They help each other with early customers and distribution. This kind of community support is what Seattle lacks.

Brentt: I just want to add a little bit to that. I think the community element here is multifaceted. When I first started coming up here, I noticed two distinct groups: the old-school, incumbent community of founders, funders, and buyers, and a new community of folks. These groups didn't cross over much—they felt like two very distinct sets. At various dinners and events, you could sense the division when people from these different groups were at the same table. It felt strange.

Regarding capital, there's diversity in terms of stage. There are significant pre-seed and seed investors, including what you and your team are building, and other smart, value-add investors. However, the funnel thins out after that. In the acceleration stage, there doesn't seem to be the same volume of dollars willing to take risks. This funding tends to pick up at early B stages when companies are more proven, but there's not enough capital willing to invest in the critical acceleration phase. This results in either capital on the sidelines or not enough support for companies at that stage.

Kirby: I think it ties into something we wanted to discuss. When our companies hit that stage, almost all of them are raising in the Bay Area. The numbers show they have to, but it can be a challenge for founders based here who aren't working in the Bay, and who don't have investors like us on their cap table to connect them. We've done many investments, and probably 30 of them have been raised from the Bay Area because we have that network. But that isn’t available to everyone.

How would you recommend founders here, who maybe don't have that advantage, get in the flow? How can they get in the flow, whether it's participating in hackathons or having get-to-know-you coffees with investors before they need the relationship?

Victoria: My advice would be, and this is a new positive phenomenon I see in Seattle, to be very thoughtful when you raise your pre-seed and take your angel check. Bring investors into your cap table who are deeply connected outside of this area and have strong functional or industry expertise. I see this starting to change.

There are three amazing pre-seed funds that I know about, and there are others I might not know. For example, Kirby, who is very networked. Andrew Peterson, who has a pre-seed fund and is super networked in cybersecurity. If you're a security founder, you should take a check from him because he knows all the cyber investors outside of the Bay Area.

Another example is Tim Chen at Essence, who is a fantastic infra investor and one of the best I've met. Taking money from him is beneficial because all the top Bay Area and global firms follow what Tim is doing.

I don’t think get-to-know-you coffee chats are worth it, that’s just my take.

Kirby: You just saved everyone $1,000… What about founders actually embedding themselves and doing their business from places like San Francisco? From my perspective, we have a team that has been there for six months. They had been wandering the desert for a year, hacking and trying to find solutions. Being in the flow down there, they've figured out what AI infra problems actually matter. They've been able to network and talk to other builders and VCs. Now, I don’t have to worry about who’s going to do their next round because they’re there and connected. So, I’ve seen it work.

Sunil: I heard you mention a founding team that was initially struggling and then moved closer to their customers. This approach is spot on. The other details about being in the right place or meeting the right people don’t matter as much. What really matters is having happy customers. If you can bootstrap or find a cost-effective way to gain happy customers, that's the key to unlocking seed capital.

When you're looking for Series A, Series C, or beyond, having happy, paying, repeat customers will help you attract investors from anywhere, whether New York or elsewhere. It's more about proving customer interest quickly.

In a pitch, I’m most interested in hearing about your product and who it’s for. I want to know if people love it, keep coming back, or if your servers are overwhelmed by demand. That’s more important than how many times we've met for coffee or how often you stay in touch. Customer traction is what truly draws my interest.

While I do invest in some cases before customer traction, like with Esper, it’s usually in areas I know really well and can anticipate customer interest. In general, my advice is to focus on your customers above all else. Don’t worry too much about staying close to investors. Listen to your customers—they are the only ones who truly matter.

Audience Q&A: What's the biggest lever, in your opinion, that will get Seattle, not to become that amazing, complete ecosystem we all want, but that will take us on that path to being the amazing startup ecosystem?

Victoria: I'm going to go with acceleration, leadership, and more pre-seed funds. Pre-seed GPs, like Isaac sitting in the room over there, are really good at guiding founders through to the next round. This is a significant change in Seattle over the last five years. And, of course, there's Kirby.

The expansion of these pre-seed funds is crucial. Hopefully, they are raising money from companies like Microsoft and Amazon, which can be really helpful for distribution. That's how I see improving distribution in Seattle.

Brentt: I'm going to go in a slightly different direction and talk about the alignment of the community. What I mean by that is, everything we've talked about—capital, customers, and talent—is all here. Over time, at events, you'll see folks dwindle, but those who are truly committed will stay. That’s my honest take on the alignment part of it.

There seems to be this divide between the incumbent tech community and the non-incumbent, newer people. This isn’t unique to Seattle. For example, in Detroit around 2011 and 2012, there were the smart Ann Arbor people and the new, also smart, downtown Detroit people. Companies like Duo Security had to bridge that gap. Once the alignment happened, great things started to occur.

By: Nate Bek

For Vivek Ladsariya, building companies is a lot like cooking.

“You eat what you make, so don't make bullshit,” he says, a mantra that has guided his career as a founder-turned-investor.

Vivek is now Managing Director at Pioneer Square Labs and GP at PSL Ventures. In the role, he helps invest out of its $100 million fund focused on Pacific Northwest tech startups. He also works with PSL’s startup studio to create new companies. Vivek covers AI, cybersecurity, infrastructure, industrial tech, and devops.

“Don't get too caught up in trying to bullshit your way around building a company,” he tells Ascend. Instead, founders should solve real problems, he says.

Before joining PSL, Vivek was a GP at San Francisco–based SineWave Ventures. Throughout his career, Vivek has invested in companies like Databricks and MindMeld (acq. Cisco). He also founded and exited his own companies: GameGarage and Moyyer Secondary Markets. Vivek was featured in Forbes’ 30 under 30 section in 2018.

Founded in 2015, PSL has raised $180 million to date for its venture fund, and about $50 million to support its startup studio that has spun out more than 35 companies including Boundless, Recurrent, SingleFile, and others.

Ascend invested alongside PSL on a number of deals, including Yesler, Meetingflow, Overland AI, Recurrent, and Iteratively.

Vivek grew up in India and did undergraduate studies at the University of Mumbai. He earned an MBA from Yale. In his off hours, he enjoys cooking with friends and being outdoors.

Vivek was kind enough to sit down with Ascend for our VC profile series, where we showcase early-stage investors from across the US. We talked in more depth about his VC passion, PSL’s unique value add for founders, and why cooking relates to investing. Read to the end for carve-outs.

*We've edited this conversation for brevity. Enjoy! — Nate 👾

Nate: Thanks for chatting with us, Vivek. What made you decide to be a professional investor? And what led to this moment?

Vivek: There was certainly no active decision to become an investor — it was something that happened by fluke. I was an entrepreneur. I'd started companies in my life before. And that's all I knew how to do and what to do. I found myself after an exit without my next company lined up, and was exploring what to do, started to make a couple of angel investments and fell into the investing world. As a result, I soon enough started to love it. Because it was a really neat way to stay engaged in the early stage ecosystem, thrive on some of that early stage startup energy, while still being able to see a breadth and range of companies. And that, to me, was very exciting.

What’s getting you the most excited these days, whether that’s AI infrastructure or specific verticals?

Horizontally, I've always focused on enterprise infrastructure. I started my career in big data, learning how to derive actionable insights from large amounts of data. This led me to invest in data analytics, data management, and data infrastructure. With every new computing shift, the types of infrastructure needed evolve. Some will be built by incumbents, but many new companies will emerge. That's where I focus a lot of my time.

Vertically, I'm excited about industries that haven't been very software-driven. I've spent time in agriculture and manufacturing, exploring opportunities there. These industries may not be large markets, but they offer great opportunities for vertical integration and driving deep value where software hasn't been prevalent. It's challenging because you need to understand the industry well to deliver precise solutions. People in agriculture, for example, buy technology for specific needs and are conscious of their spend.

As an investor, I find it exciting to learn in-depth about these industries. While most industries today are software-driven, the key question is whether they are leveraging the most modern technology and where such technology can be applied.

One of the reasons I got into journalism, and now VC, is what you mentioned on the vertical front of learning about industries that are foreign to me. I remember at GeekWire I wrote about a pasta company. And, yesterday, I went deep into proptech. There's just so many opportunities to find ways that software can help a specific industry and their pain points — it's a cool motivating factor.

It's funny, right? Back in 2011, Marc Andreessen wrote "Software is eating the world." I think it was probably true for at least 10 years before he wrote it. It's been 13 years since then, and it's still very true. I think it will be true for the next couple of decades.

Software is eating the world, and it's our job to find the little crevices that haven’t been chewed off yet. Switching gears, what's your pitch to founders? And why should they want you on their cap table?

There's obviously a lot of nuance here, depending on the space, the co-founders, the history with the founder, and so on. Sometimes you’ve known a founder for 20 years, and there isn’t much of a pitch. But when that's not the case, there is a firm pitch because you're working with PSL as a firm and me individually as a partner. There are unique advantages to both.

PSL is exciting because we are both a company builder and an investor. This dual role allows us to understand the nuances of building companies. All partners on the team are deep operators. For an entrepreneur, partnering with a firm that truly understands the daily grind of building a company is invaluable. We at PSL share our learnings regularly and routinely.

As for me, I’ve built and sold companies before, and I leverage that experience to help founders. I pride myself on being the first phone call my portfolio companies make in tough times. Startups are hard, and I want to be the person they want to call, not just feel pressured to call. I work hard to be able to solve critical problems and be a great listener, supporter, and advocate through the challenging times that are inevitable in every startup journey. This was important to me when I was building companies, and I think it's crucial for founders today. Most of the founders I work with would probably say I’m their first phone call when things get tough.

It's a good value add. On the firm side, what's interesting is that you often hear about someone who has founder-operator experience. What's unique about PSL is that you guys are not just relying on experience from 20 years ago; you're actively building companies right now. You're using the latest technology, the newest back-end tools, and exploring emerging opportunities. You are actively iterating and hacking together with the founders…

Not many founders get the luxury of meeting with investors to discuss how the investor is in real time using this particular RAG model to ingest data, or to search across enterprise data. I think that is really unique.

Why come from the Bay Area to Seattle? What drew you here? What opportunities are you seeing, and where do they lie right now?

When I first started evaluating Seattle, I saw it as a great opportunity—an underpriced one—with incredibly deep tech talent. This talent is building in spaces and infrastructure that I care about. It quickly became evident that Seattle isn't just a good opportunity; it might be the best location for certain types of technologies. While not for all startup building, for core infrastructure tech companies, Seattle is one of the best markets globally. The talent depth here is incredible, with some of the largest tech companies headquartered or having significant engineering hubs in the city. This creates a magnet for tech talent like no other place.

Despite being just an hour and a half flight away in San Francisco, I was far removed from the Seattle tech scene for years. Now, I see a real opportunity to build a bridge between San Francisco and Seattle, which can be a powerful way to innovate and create category-defining companies.

The bridge between the Bay Area and Seattle is crucial. At Ascend, we often discuss how Seattle has incredible engineering talent and birthed many of the world's biggest companies. However, it lacks growth-stage capital and some of the growth marketers, angels, or advisors found in the Bay Area. To scale a startup effectively, it's essential to build in Seattle while tapping into the capital and expertise available in hubs like San Francisco.

You nailed it. That's an important aspect—it doesn't need to be geographically isolated. The strengths of Seattle and the Bay Area can come together to form something powerful and unique. To me, that's where the real opportunity lies.

What’s the bear case?

To me, not being great at certain sectors isn't necessarily a bear case. Not every region needs to excel at everything. If we generally don't build world-class consumer companies, that's fine; they can be built elsewhere. We should focus on our strengths. The real risk is not leveraging those strengths to their maximum potential. This means not bringing the rest of the world along on our journey. If we build in isolation, we won't create large, impactful companies. Growth capital isn't abundant here; it's distributed across the country and the world. We need to engage these external resources sooner and more frequently.

Another risk is brand building. Even if we excel in non-consumer sectors, we need to solidify and promote our brand globally. The Bay Area is often too boastful, while Seattle tends to be too reserved. The sweet spot lies in building a highly credible and sincere brand while ensuring we publicize and take credit for our achievements.

What are you reading these days? What sources are filling you in on the latest RAG updates?

We invest at the earliest stages, often mere weeks from a company's formation. This requires staying up-to-date well before a company's inception, which poses unique challenges. One approach for me has been being deeply involved in the open-source community. I keep track of promising open-source projects and those gaining momentum.

Additionally, I spend time reading research papers in the fields I care about. Researchers working at the cutting edge, or as one of my friends likes to say, the "jagged edge" of technology, often develop technologies that will commercialize in a year or two.

Practically, finding and meeting entrepreneurs involves engaging with universities and key team leaders at major tech companies like Microsoft, Amazon, Google. By being a thought partner and staying ingrained in the open-source community and research trends, I position myself as a natural choice for these leaders when they consider starting a company.

Fun question time! Spotify or Apple Music? What song is getting the most play?

I am definitely a Spotify person, mostly because that's where my family plan is. I just use whatever my wife uses. A song I'm listening to a lot these days is "Let's Be Still" by The Head and the Heart. I play it every morning on my drive. It's a centering song that helps me pause before the chaos of the day. I play it every morning, but my favorite song changes pretty often.

Favorite shoe?

I have these Fila squash shoes from 2018 that are completely in tatters and falling apart at the edges. But I wear them every morning when I work out because they feel like my Samurai shoes. Every time I step into them, I feel like I'm gearing up as a samurai. Outside of that, on an everyday basis, I just wear whatever shoes I find.

I love it. The routine is the important part… Now’s your time to shine. What’s your go-to ingredients in the kitchen and how do you make the case that cooking and investing are similar?

I love to cook, and my favorite ingredient, without contest, is garlic. I probably overuse it according to others, but I think it’s not used enough in most cooking. Garlic is a core part of my pantry at all times.

Interestingly, I see a lot of similarities between cooking and investing or company building. The quality of the ingredients is paramount. In cooking, if you start with great ingredients, you just have to avoid messing up too much to end up with a good dish. Similarly, in investing, the "ingredients" are the people. Focus on high-quality people, and you’re likely to build a successful company.

A friend of mine used to say, "You eat what you make, so don’t make bullshit." Eventually everything comes to roost. Everything gets put on a plate and you have to consume it. Don't get too caught up in trying to bullshit your way around building a company — build something real and solve a real problem. And, eventually, you’ll have something good to eat.

By: Nate Bek

What makes pre-seed investing so paradoxical?

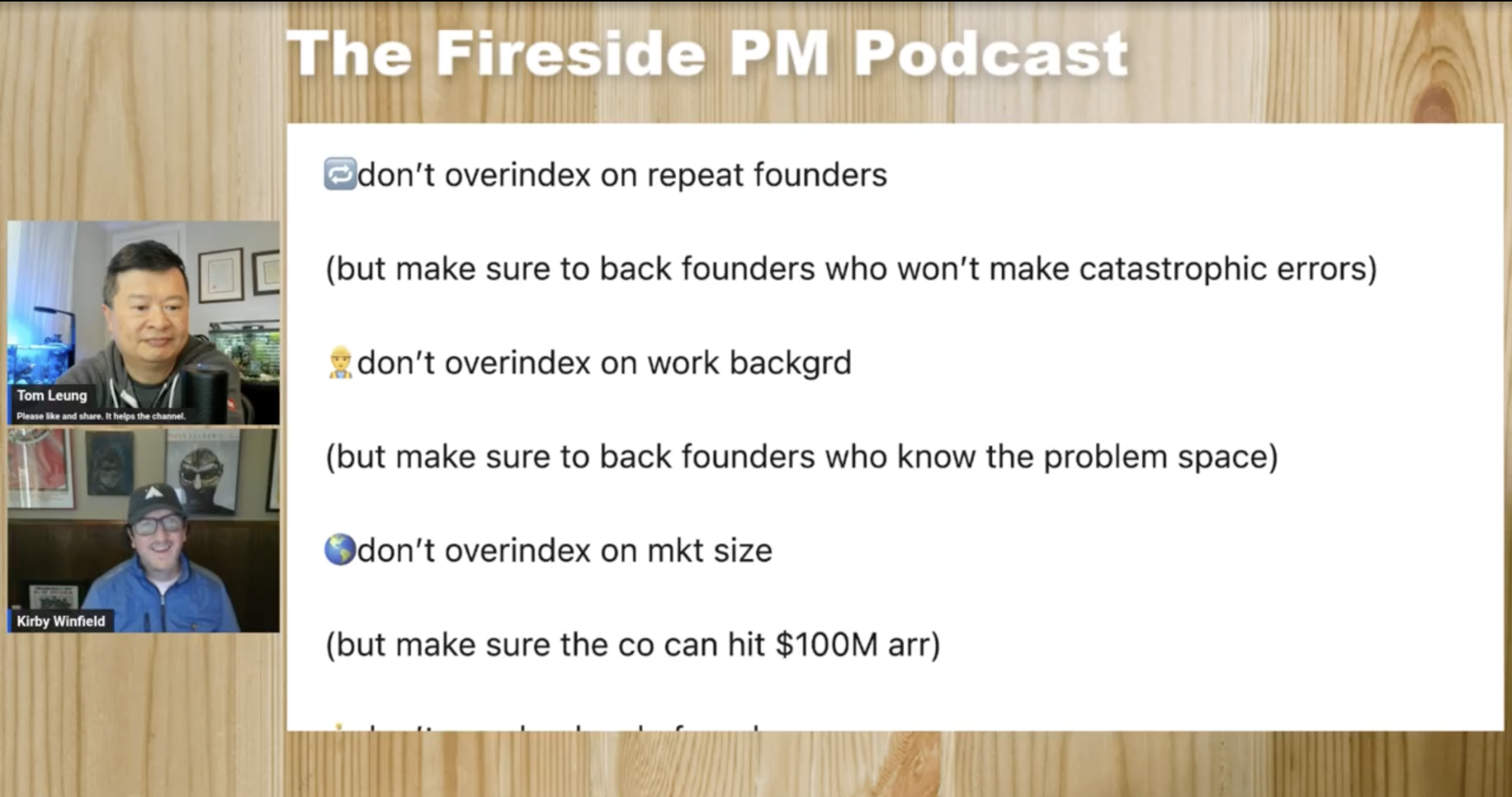

During a live Q&A session, Tom Leung, host of "The Fireside PM Podcast," posed this question to Kirby Winfield. Inspired by his LinkedIn post — which highlights several contradictions in pre-seed investing — Tom asked Kirby to methodically break down his insights, starting with, "Don’t over-index on pedigree," and, "Make sure to back PhDs."

“As an investor, I'm constantly trying to understand my mental algorithm,” Kirby says. "I started thinking, ‘I'll just use my gut. I'll know it when I see it.’ But then I unpacked my gut instincts and questioned what’s informing them… For every gut reaction you lean into, there's an equally valid instinct leaning the other way.”

Throughout the interview, Kirby untangles these paradoxes and shares his experiences, line by line.

Here are some key takeaways:

Gut instincts matter — Pre-seed investing is complex, but gut instincts play a crucial role. Kirby says, “You balance everything, try to figure it out, then realize, ‘Yeah, it's your gut.’” Refining these instincts helps in evaluating founders effectively.

Credentials aren’t everything — A Stanford PhD doesn’t guarantee success. Kirby emphasizes, “If credentials were the key, every Stanford PhD would walk out with $50 million from a VC.” Focus on a founder’s ability to find product-market fit, tell a compelling story, hire top talent, and execute their vision.

Upstream biases — Later-stage investors often rely on patterns and biases. Kirby says, “You have to be very thoughtful about how you navigate it.” Overcoming these biases requires backing founders who can create massive outcomes, regardless of their background.

Charisma vs. substance — Charisma helps in pitching but can mask deeper issues. Kirby says, “There’s a fine line between charisma and charlatanism.” Founders need more than just sales skills to succeed.

Revenue vs. customer love — Early success is about user love, not revenue. Kirby says, “It just matters how much the people using the product love the product.” Look for passionate customers.

Background vs. problem space — Founder-market fit is crucial. Direct problem experience is key, not just industry background.

Market size vs. ambition — Great founders can turn small markets into big opportunities. Kirby says, “The biggest misses I have are ones where I loved the founder but hated the market.” Focus on the founder’s ambition and vision.

Keep reading for the full Q&A transcript, edited for brevity and clarity.

Tom: We are back with the Fireside PM Podcast, and I have Kirby Winfield from the great city of Seattle.

Kirby: It’s a beautiful blue sky, spring day, 60 degrees. We’re coming around that time of year where we get the rewards of having suffered through 120 days straight without sun.

You do have an amazing income tax in Washington State...

Don’t tell the legislature. Life’s still good. We still welcome a lot of our brothers and sisters from California who find their way up to our haven.

It's a trade-off, for sure. And there is no other place that is quite as beautiful as Seattle on a nice day. It's magical. Well, for those who don't know you, Kirby, why don't you just give us a little bit of an introduction, and then we can get into the meat of the conversation about pre-seed investing?

I was born and raised in Seattle. I went back east for college and graduated in 1996. After college, I moved to Manhattan to pursue a career in advertising.

Three months later, a friend called and said, "Hey, I'm starting an internet company. Come back to Seattle." So I did. I was the sixth employee at GoToNet and eventually ran marketing. We drove a third of Google's traffic and became a top 10 internet destination. We went public, and I was a 24-year-old running marketing for a $4 billion company.

That was my introduction to startups. I made every mistake in the book, but it was a forgiving time. I worked for two great co-founders, and luckily, it went well. We exited in 2000 and started another company, Marchex, where I was on the founding team. We also took it public and did a $200 million secondary offering. We bought many domain names, and I ran that business, growing it from $5 million to $50 million in just over two years.

I always say, “I mistook my good fortune for talent.” Like many, I thought, "These guys are taking companies public. I can do that." I believed I could be a CEO. I took over a venture-backed startup that raised $18 million and quickly found out it was built on questionable traffic. We pivoted to an analytics big data play, laid off two-thirds of the staff, recapitalized the company, and spent six months on Sand Hill Road shopping the deal. Two VCs were interested, but the existing VC crammed down the other. That was my introduction to venture capital. We sold the company a year later with a great outcome.

I did one more startup as a founder, raising a couple million dollars for a travel app that we sold to Expedia. Twenty years, four companies, four exits. But the ones I ran lacked the exit value of those where I just bet on the right founders.

After that last exit, I decided to switch it up and bet on founders. I did angel investing off my own balance sheet because it was at the intersection of what I liked and was good at. Most of my operating career involved tasks I didn't enjoy or excel at. As an investor, I focused on what I loved: marketing, networking, connecting people, events, and exchanging ideas. I learned from founders and offered valuable insights, having made many mistakes and had some successes.

Angel investing didn’t feel like a job. Founders appreciated my feedback, and I helped with customer introductions, hiring, and raising capital. Our mutual friend Oren Etzioni invited me to help spin out an incubator program. Eventually, LPs showed interest in a fund. I raised my first fund in 2019 and a second in 2021.

I've recently started getting into angel investing, and I definitely hear you that it is so fun talking to founders. You get a little vicarious thrill, knowing that they're on the hunt. Hopefully, I enjoy sharing some war stories and saying, "Hey, look, I know where you’re coming from. This is what I did, and some lessons I learned the hard way."

It's valuable because it’s something you can do that higher-level investors can't empathize with or share useful experiences about, beyond investment or board management. They've seen the strategy, but for the zero-to-one journey, you don't want a growth investor. You want a founder. You want someone who's been there and done that.

Well, Kirby, you did a post on LinkedIn that caught my eye. I'm going to share it on the screen here, and it has a very catchy start, which is, "Hey, pre-seed investing is easy," and then you go through a bunch of learnings. I thought it might be fun for us to go through each one and hear a little bit of the story behind it and how you arrived at that insight. The first one is, "Don't over-index on pedigree, but make sure to back PhDs." Can you say more about that?

As an investor, I'm constantly trying to understand my mental algorithm. It's like observing my own thinking process. I want to know why I’m leaning towards or away from certain founders. I map this to the data from the 80 investments we've made so far.

I started thinking, "I'll just use my gut. I'll know it when I see it." But then I unpacked my gut instincts and questioned what's informing them. What biases do I have? If you're honest and intellectually candid, you realize that for every gut instinct you lean into, there's an equally valid instinct leaning the other way. It's confounding.

It's like the midwit peak meme: the simpleton says a thing, the midwit overcomplicates it, and the genius circles back to the simpleton’s point. That's been my journey. You balance everything, try to figure it out, then realize, “Yeah, it's your gut.” This process of unpacking helps refine your mental model for evaluating founders.

You don't want to back people just because they worked at certain companies, held specific jobs, or attended prestigious universities. Outcomes are distributed more broadly than that. If credentials were the key, every Stanford PhD would walk out with $50 million from a VC. But credentials don't make someone a founder. Can they hack their way to product-market fit? Can they tell a compelling story, hire top talent, raise funds, get press, and close deals? None of this is guaranteed by a PhD.

At the same time, my job is to help founders raise funds from big venture capital firms, which often back Stanford PhDs. It might feel safer to back someone with certain credentials because they match patterns seen from later-stage investors. But that's not the right approach for pre-seed investing.

Our portfolio includes dropouts from state universities and Stanford PhDs. I think the job of investing at this stage is to curate… Investing at this stage is like being a DJ at a party. You don’t just play old-school hip-hop; you create an experience that appeals to everyone. Investing in startups requires a broad surface area, beyond any one credential set or market slice.

Let me ask you a couple of follow-up questions on the pedigree front. I’ve actually heard people take that argument even further and say, “You definitely don’t want the Stanford people, and you definitely don’t want the Google or Facebook people, because they haven’t suffered, and they don’t know how to make something out of nothing.” And if you got a Stanford PhD, you’ve been on a pretty golden path. What’s your take on that? Do you actually ding people?

It depends on who’s holding the piece of paper. If you moved here from rural India at 12, fought through the public school system, made it to college, and then leveraged that into a PhD at a great school, that's very different from someone whose parents were PhDs in California, with one running a tech company. It's about evaluating the whole person.

Some people have been at AWS for eight years because they were challenged and stimulated by the software engineering work and needed to build a nest egg. Now they want to start a company. Others have worked in machine learning at AWS for eight years and should stay there. My job is to figure out the difference between these two people who look identical on paper.

How do you do that? If they do look identical on paper, how do you tell the ones that should stay versus the ones that should go for it?

If I could bottle that, I could sell it. If I knew I had it — I just don’t know. I’ve built a Google form to score founders on different axis, but it doesn’t really matter whether I use it or not. At the end of the day, you get a feel for the person and their reasons for what they’re doing, the urgency they feel, the vision they have to build something meaningful, and their understanding of the journey. You evaluate their ability to execute on those things. That’s what matters, and that’s what we try to figure out.

Another follow-up question: you mentioned that sometimes downstream investors like that pedigree, or they put a lot of money against Stanford PhDs. Have you seen a case where you back a less conventional founder who’s producing a really legit, great growing business, and they encounter more headwinds than they should have because of that lack of resume, or do the numbers eventually speak for themselves?

It’s not companies that get parabolic growth, or they start to look a certain way from the numbers, and they have the right logos, and they’re in the right market. Those companies get funded.

It’s more the companies that, if it were a female founder who’s been at Microsoft for 18 years and is non-technical, or a male PhD from Berkeley, both companies are doing okay. But to be venture-backable at Series A, you have to be really great.

Historically, that’s always been the case, and then it wasn’t for a little bit, but now it is again. What does great look like? It can be that you’ve got good traction, plus a credential that takes you over the line. If you’re good but don’t have the credential that takes you over the line, or don’t have a profile that historically gets backed a lot, then you don’t clear the line.

People will give you the benefit of the doubt more if there’s a reason to give you the benefit of the doubt. I get it. I have a freaking English major from Middlebury College; my pedigree academically isn’t going to give me the benefit of the doubt. If I’m looking at me, then there’s someone similar but with an additional set of interesting credentials that signify their intelligence and depth of knowledge and ability to focus and think critically that I don’t have… Well, I would probably invest more in that person, too. That’s data. I’m not going to say that you understand why it happens.

It sounds like if your company’s killing it, then you could not even have a college degree. It’s like, “Wow, that chart is clear. It’s parabolic. Let’s pour gas on this.” But in many cases, they are in that gray area, and that edge goes to patterns that investors are comfortable with or have seen success with in the past.

They’re comfortable, probably because they at least think they have data that shows they’ll feel good about that bet and will make their investors money. The only reason they’re doing this is to make their investors money. There’s no other reason they’re doing this. That’s what VCs do.

The challenge exists in trying to unpack how much of that is a methodology. How much of it is PhDs making us more money because we give PhDs more money? It may be that it’s correlation, not causation, and that would be the argument. Certainly, we believe that talent is distributed equally. Opportunity isn’t.

We’re not an impact fund, but we have folks from every kind of background as founders in our portfolio. We’re on that side of that discussion. Breaking the cycle of, we’ve done this and it works, so we should keep doing it, even if you don’t know how it would work if you didn’t do it.

There’s no real A/B test at the growth stage. This is why it comes down to LP pressure. If institutional LPs pressure GPs to make different decisions at the growth stage, then investors at my stage are freer to do what we want. I’ve talked to female VCs at seed and Series A who know the data and see it, so they’re making investments, and they’re like, “Well, I want to back women, but 2% of venture dollars go to women. Am I going to be the one to change that, or am I just going to back a bunch of women that don’t get back to Series B and C?” It’s insidious.

It’s not a lack of desire on the part of early-stage investors to change it. It’s a lack of incentive at the later stage to be open to it. This is not something I pound the table about, but I’m just sharing my personal views about it. It’s something most people will not talk about. My goal is to back founders, regardless of their background, who can create that parabolic company. I don’t care, even if later-stage people make decisions based on biases or bad data. I don’t think it matters because it would be irresponsible of me to invest this way if I did think it mattered.

I’m backing people because it’s 2024, and I’m backing people who can create massive outcomes no matter who they are.

If you believe that you’re being meritocratic and completely data-driven, but you worry that later-stage investors aren’t, that creates a disincentive for you to necessarily back the best founder because you have to consider that part of being a great founder is the ability to raise capital down the line.

You have to be very thoughtful about how you navigate it. This woman, who is a Valley investor I was mentioning, she’s a stage later than me but still early. That was her conundrum. I won’t go founder by founder, but we have founders in Fund II who are from underrepresented backgrounds in venture who have Stanford PhDs.

My approach is simple: I don’t care where you’re from, who you sleep with, or what you do in your spare time. If there's something spectacular about you that maps to the problem you're trying to solve, I want to back you. That's the way everyone should approach it. But I’m just one person.

“I think TAM (Total Addressable Market) is an excuse people use to avoid investing in founders they don’t like.”

Don’t over-index on charisma. What I heard from you earlier in our conversation was, “Hey, you want someone that can raise more than they maybe should and hire people that shouldn’t join them and convince customers to buy stuff that’s not quite ready.” It sounds like charisma is a really great thing to have. What do you mean by not over-indexing on it?

There’s a fine line between charisma and charlatanism. You don’t want to just back a really good salesperson. It’s very hard to invest in founders with sales backgrounds, at least for me, because they’re all really good at selling you, but there’s a lot about the job that has nothing to do with selling, and it’s the same for founders. You have to be thoughtful.

The corollary to that is Seattle investors, when they see a Valley founder pitching them, they just want to give them money because Valley founders are so much more polished than founders in other markets because they’ve had so many more swings. They’ve worked at so many different startups. The startup culture is in the water there. They probably have five advisors who have founded companies already. You see that as an investor who doesn’t always see it and think, “Oh my gosh, this is the best founder in the world.” Well, no. No more so than they would be up here. They’re just better at pitching.

You can’t just back people who can pitch, but it’s very hard to back people who can’t pitch, even if they’ve got other skills.

“Don’t over-index on revenue, but make sure to back founders who can get profitable.”

At the earliest stage, it doesn’t matter whether you have $10,000 in revenue or $100,000 in revenue. It just matters how much the people using the product love the product. How sad would they be if it went away?

I care much more about logos than revenue. Do you have five recognizable venture-backed startups as customers, and do they love what you’re giving them? That matters way more than revenue. To raise a seed round now, you need $500,000 in revenue. Two years ago, you needed a pre-seed and two co-founders.

I’d rather have a founder who has customers and who absolutely finds their offering indispensable versus the dollar amount. What about repeat founders? “Don’t over-index on them, but make sure to back ones who won’t make catastrophic errors.”

One reason I wasn't a great founder was my cynicism and reliance on a playbook. Repeat founders can fall into that trap. The advice often is to back really young founders who don’t know what they don’t know. They'll run through walls if pointed in the right direction and eventually find the goal.

A repeat founder might move slower and have more to lose. First-time founders, especially recent college graduates, don't. Their work rate is incredible. But first-time founders sometimes run off a cliff because they weren’t looking down. They might bring on the wrong investor, hire the wrong person, or face co-founder issues.

The point is you can choose either and encounter problems with both. We back both kinds of founders.

“Don’t over-index on work background, but make sure to back founders who know the problem space?”

Just because someone was a data scientist at GitHub doesn't mean they'll automatically build a successful developer tools modern data stack technology. Product managers often want to start a company because they handle many tasks, but that's not the ideal archetype. They often lack direct responsibility.

We constantly tell founders we want founder-market fit. We want you to have a unique insight that nobody else has. The only way to have that is if you’re coming from the space where the problem exists and have worked on it directly.

There’s data supporting both sides. Yes, a successful founder might have come from WhatsApp and started a billion-dollar app analytics company. That's founder-market fit. But they could have easily been a crappy founder for other reasons. The first question is, are they going to be good at founding and growing a company? Everything else helps you feel more comfortable backing them.

It’s interesting how your post talks about these common characteristics, and for each one, there are examples and counterexamples for the rule. Ultimately, you just have to make a call. It’s not going to fit one pattern.

It's infuriating, and nobody explained this to me when I started as a venture capital investor. People often talk about luck. Many smart, hard-working people are in this job, and some get lucky while others don’t. You have to put yourself in the way of luck. You do that by getting the best deal flow, picking the best deals, and winning the deals you pick. Those are the three things that matter in venture capital. But the picking part is the hardest because of these challenges.

Market size. Some markets might be too small. I was listening to Jason Calacanis live stream, and someone pitched a marketplace for collectibles for tabletop games. I was like, wow, I don’t know how big that market is. What’s your take on how big the TAM needs to be?

I think TAM (Total Addressable Market) is an excuse people use to avoid investing in founders they don’t like. TAM is code for ambition. Amazon’s initial TAM was people who wanted to buy duck decoys. Then it was books, which was a shrinking TAM. Remember Justin.TV?

Oh, yeah.

We ran ads on that and got in trouble for it because it was pretty wild west. The thing is, with a great founder, the thing doesn’t have to be the thing. The biggest misses I have are ones where I loved the founder but hated the market. If you love the founder, find a way to like the market.

If you love the founder and hate the market, have you ever convinced the founder to look at another market, or do you just go with it?

No, because you don’t want to back the founder who will change their mind based on your feedback. So you just go. There are still deals we won’t do, like biotech. We won’t even take the meeting. There’s a marketplace-adjacent deal I’m looking at now, and we don’t do marketplaces anymore. We did it for Fund I, won’t do it in Fund II, but I like the founder. There’s a difference between market size and markets you don’t like. I don’t think market size matters. I do think there are markets I’m allergic to. Travel. Ad tech. Not surprisingly, markets I’ve operated in.

TAM is usually about ambition. If you’re not telling me why it’s going to be monstrously big eventually, your ambition is to get a small slice of a small market. Unless you’re a dynamic founder, I’m not interested.

Why did you change your mind about marketplaces?

All the easy ones have been done. They’re slow. There’s always margin compression and a leaky bucket problem. Lots of reasons.

Don’t ever back solo founders, but make sure to back singular visionaries.

People will back solo founders. Some investors won’t back solo founders because they like to have two people making decisions. I believe I’ll make better decisions by myself. Some investors don’t like that and won’t invest.

Don’t work with assholes, but make sure to back disagreeable ones.